Looking at the four major public blockchains from an RPC standpoint, how do BTC, SOL, BNB, and ETH perform?

Original Author: Murphy, On-chain Data Analyst

——You don't know how bad it is until you compare it to something else

The Realized Price (RPC) is a concept frequently used in on-chain data. Before understanding RPC, one must first understand Realized Cap (RC). RC is the sum of all coins valued at their last move price.

RC excludes factors such as lost or long-term non-circulating coins, better reflecting the true stored value in the entire blockchain network;

Dividing RC by the current total circulating supply gives us RPC. The higher the price at which tokens are sold (moved), the more subsequent funding it implies, and vice versa. In other words, only continuous buying at high prices in actual gold and silver can raise RPC. Therefore, it is the most direct basis for observing capital inflows.

At the same time, RPC is also considered the average cost basis. Whenever a pullback occurs, RPC can play a significant support role. Once the price falls below RPC, it means the average position is at a loss. At this point, the asset price is "undervalued," attracting more bottom-fishing funds when the risk-to-reward ratio appears, gradually forming a bottom range.

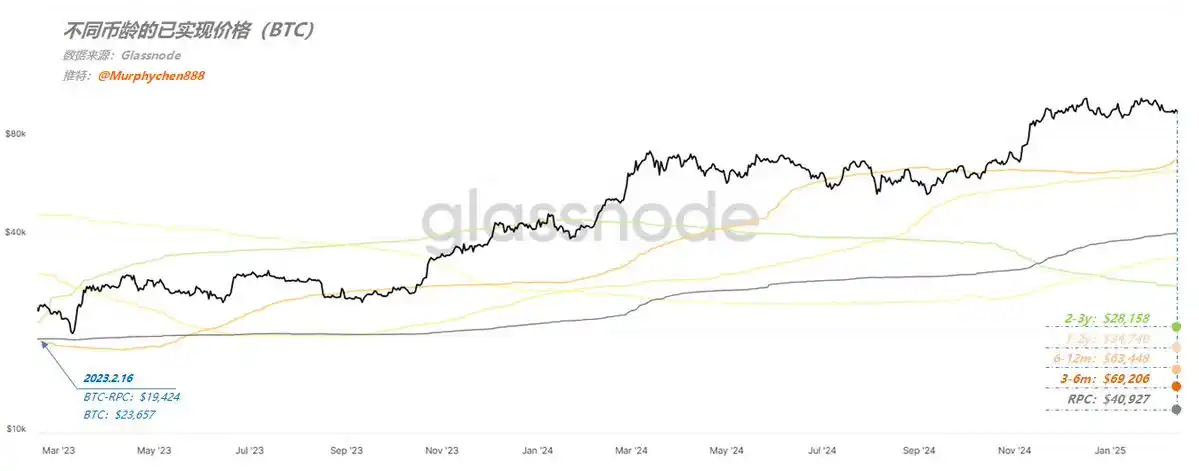

· BTC

Figure 1 shows the RPC data for BTC at different coin ages (holding times). It can be seen that among the four Long-Term Holder (LTH) groups, the longer the time held, the lower the average cost. The cost for 3-6 months (3-6m) is $69,200; for 2-3 years (2-3y) the cost is $28,158; in other words, even if one day BTC falls back to $30,000 during a bear market, these LTH groups are still profitable.

(Figure 1)

As of February 13th, BTC's RPC is $40,927, based on the current price of $96,600, investors still have an average of 136% unrealized gains, providing an excellent holding experience! Therefore, whenever BTC's price fluctuates, there is little panic selling pressure, and no chain reaction is triggered. This is also one reason why BTC in this cycle "doesn't drop too deeply." With such a low RPC, it is clearly not a reference price to support during a bull market cycle correction, but it can serve as a judgment standard for the bottom phase of a bear market cycle.

On 2023.2.16, the RPC of BTC was $19,424, a 210% increase over 2 years; during the same period, the price of BTC rose from $23,600 to $96,600, a 409% increase. The price increase far exceeded the increase in absorbed capital, indicating that in addition to capital, BTC also attracted more mainstream sentiment value (high market attention).

· SOL

Figure 2 shows the RPC data for SOL at different coin ages. In the past 2 years, SOL investors have had a very positive holding experience. It can be seen that the average cost of all long-term coin-holding groups is lower than the current SOL price. The cost for 3-6 months is $167, and for 2-3 years, it is $71;

(Figure 2)

As of February 13, SOL's RPC was $141; based on the current price of $194, investors still have an average of 37% unrealized gains. From this point of view, the stability of the SOL chip structure is far inferior to that of BTC. However, conversely, $141 is also a very strong support level. As long as there is a bull market consensus, the closer it is to this line, the weaker the selling pressure and the stronger the bottom-fishing sentiment.

On 2023.2.16, SOL's RPC was $39, making it the only mainstream coin at that time with a spot price lower than the RPC. In other words, SOL at this time was one of the most undervalued among several mainstream coins, offering the best cost-performance ratio. Over the course of 2 years, the RPC increased by 361%; during the same period, the price of SOL rose from $22 to $195, an 886% increase. Once again, the price increase far exceeded the increase in absorbed capital (better than BTC), indicating that in this cycle, SOL has also gained very high market attention.

· BNB

Figure 3 shows the RPC data for BNB at different coin ages. As the only token empowered by Binance and BNB Chain, it is truly deserving of the word "mainstream." Therefore, let's also look at its data performance.

(Figure 3)

The cost of 3-6m is $575, and the cost of 2-3y is $301; similarly, the average cost of all long-term holders must be below the current BNB price. There is a detail that, from February 5th to February 8th, BNB's price dropped to around $570 right at the support of the 6-12m RPC line, and then started to rebound.

As of February 13th, BNB's RPC is $495; based on the current price of $665, investors still have an average of 34% unrealized gains. However, we can observe that between October 4, 2024, and October 7, 2024, BNB's RPC suddenly surged from $206 to $463.

This data is very unusual and rarely seen in other mainstream coins with relatively evenly distributed chips. It also indirectly reflects the uniqueness of BNB's chip distribution. Only when a large number of chips reaching a certain circulation percentage suddenly move at a high level will it cause an abnormal RPC. Therefore, whether the current RPC of $495 can provide support is currently difficult to evaluate (the data may be interfered with).

On February 16, 2023, BNB's RPC was $81, which was much lower than the spot price of BNB at the time, $304; therefore, in terms of cost-effectiveness at that time, it was not as good as SOL or BTC. However, if the benefits of holding BNB such as Launchpool, Megadrop, and HODLer rewards are taken into account, the situation might be different.

· ETH

Figure 4 shows the RPC data of ETH at different coin ages. I placed ETH's data last because its data performance is the least favorable compared to the previous three.

(Figure 4)

The cost of 3-6m is $2,923, and the cost of 6-12m is $3,088; in other words, ETH is currently the only mainstream coin where investors holding for 12 months are still on average at a loss.

As of February 13th, ETH's RPC is $2,104, which coincides with the strong support formed at the lowest point on February 3rd (after the sharp drop). Based on the current price of $2,700, investors only have an average unrealized gain of 24%. This percentage is lower than both SOL and BNB, and significantly lower than BTC.

On February 16, 2023, ETH's RPC was $1,482; with a growth of 142% in two years; during the same period, ETH's price increased from $1,639 to $2,700, a growth of 164%. The price increase is almost the same as the increase in absorbed capital, indicating that in this cycle, ETH has the lowest emotional value. Or, compared to BTC and SOL, the market's expectation value for ETH is the lowest.

-----------------------------------------

· Summary

1. In terms of the stability of the chip structure, BTC is much better than other mainstream coins. The long-term holding group currently has an average of 136% unrealized gains. SOL and BNB are similar, at 37% and 34% respectively; ETH is the lowest, at only 24%. This means that the current spot price of ETH is closest to the average cost basis, and ETH holders have the worst holding experience. Once the price falls below this support level, it could easily trigger a chain reaction.

2. Comparing the price increase and capital absorption increase in the past 2 years, BTC and SOL have received more emotional hype, or higher expectations.

3. Due to abnormal RPC data for BNB generated in October 2024, the current RPC cannot determine if it has been tampered with. If not, then the current BNB holders also have a very good holding experience. At the same time, holding BNB allows for additional monthly mining rewards or airdrop benefits, which is a plus.

4. Lastly, there is ETH... How should I evaluate ETH? As one of the only two crypto assets approved through an ETF, it is high quality. However, various performances of the Ethereum Foundation leave much to be desired. Vitalik, as the founder, is undoubtedly a brilliant developer, but at the moment, he may not be a qualified leader.

PS: If anyone is interested in knowing the RPC support level data for other coins, you can leave a comment in the comment section. If I can find it, I will reply one by one.

-----------------------------------------

My sharing is for learning and communication purposes only, not as investment advice

You may also like

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.