AI Memory Supercycle Debate: Why Big Tech's Margin Panic Just Confirmed SanDisk's NAND Advantage

Key Takeaways

- Apple, Microsoft, and other major consumer tech companies have been forced to raise product prices dramatically in 2026, with Apple hiking Mac and iPad prices by up to $300 on June 25 and calling the memory shortage "unavoidable," while Microsoft raised its Surface Pro price by roughly 50%, from $999 to $1,499. These actions from the most powerful supply chain negotiators in the world are the strongest possible external confirmation that NAND pricing power is structural, not cyclical.

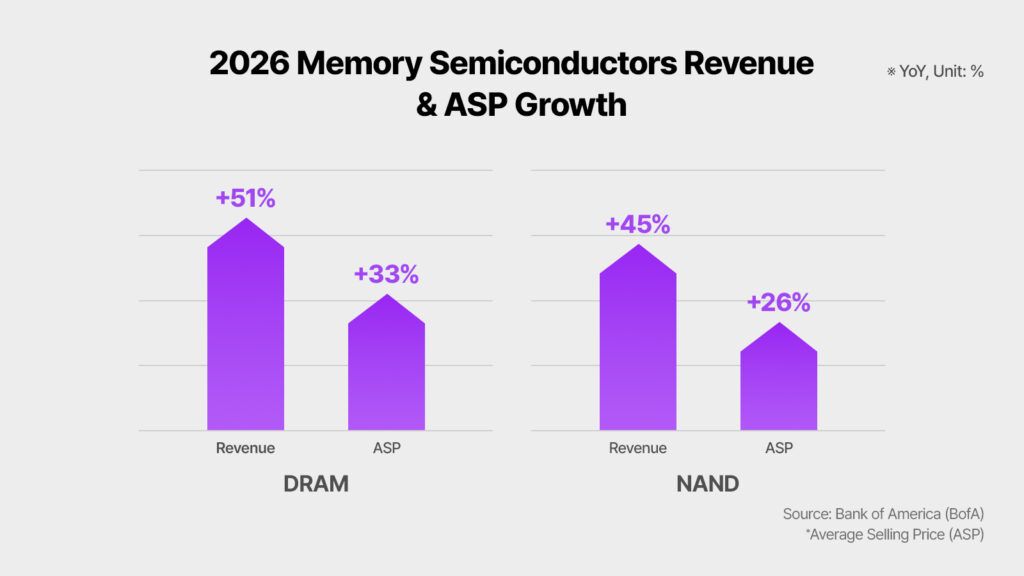

- The root cause is a zero-sum reallocation of global silicon wafer capacity: every wafer Samsung, SK Hynix, and Micron redirect toward high-bandwidth memory for AI accelerators is a wafer removed from the NAND and consumer DRAM pipeline, and IDC forecasts 2026 NAND supply growth at just 17%, well below the historical norm of 20-30%.

- S&P Global Ratings, Morgan Stanley, and JPMorgan have all issued warnings that this scarcity will persist well beyond 2026, with S&P forecasting elevated memory prices through at least 2028 and JPMorgan estimating that DRAM and NAND could climb from roughly 10-15% of iPhone component costs today to more than 45% by 2027.

- SanDisk reported Q3 FY2026 revenue of $5.95 billion, up 251% year-over-year, with non-GAAP EPS of $23.41 against analyst estimates of approximately $14, a 60% beat, reflecting the pricing power generated by its pure-play NAND position, fully booked 2026 capacity, and $42 billion in secured long-term agreements.

- Bernstein raised its SNDK price target to $3,000 with an Outperform rating, citing SanDisk's LTA contract advantage over Micron as evidence that the company has structurally insulated a portion of its earnings from spot-price volatility.

- The word "monopoly" in this context requires precision: SanDisk does not literally control 100% of the NAND market. But as the only major US-listed, pure-play NAND supplier, freed from the conglomerate discount of a combined HDD business and backed by the most complete set of AI-oriented long-term supply agreements among Western NAND makers, it occupies a market position that no direct US-listed peer currently mirrors.

The "AI Memory Supercycle" has been described as everything from the most powerful structural trade of 2026 to an overextended bubble propped up by narrative momentum. The debate intensified sharply during the last week of June 2026 when Apple, a company that has famously absorbed component cost swings rather than pass them to consumers for most of the past decade, announced immediate price hikes across its Mac, iPad, and accessory lineup, citing memory and storage costs it called "unavoidable" and "unsustainable." This wasn't a small adjustment; the Mac Studio M3 Ultra alone rose $1,300. At exactly the same moment, Bernstein analyst Mark Newman raised his price target on SanDisk to $3,000, the highest on Wall Street among major firms, citing the company's long-term agreement structure as a hidden competitive advantage over Micron. The collision of these two data points, Apple's forced admission that it cannot outrun NAND costs, and Wall Street's most bullish institutional target on the sector's purest play, crystallized what the AI memory supercycle debate is actually about: not whether demand is real, but whether pricing power will last long enough to justify valuations, and whether SanDisk is uniquely positioned to benefit even if it does.

If you want to position yourself to act on AI memory sector moves quickly as this debate resolves, you can create a free account through WEEX and start monitoring SNDK alongside the broader semiconductor landscape in real time.

SNDK USDT is now available on WEEX.

The Zero-Sum Wafer Game: Why Big Tech's Pain Is SanDisk's Gain

Understanding the AI memory supercycle requires understanding a single physical constraint: semiconductor fabrication clean rooms have a fixed capacity, and every wafer dedicated to one product is a wafer unavailable for another. Since 2023, hyperscalers including Microsoft, Google, Meta, and Amazon have collectively committed hundreds of billions of dollars to AI data center buildout, creating relentless demand for high-bandwidth memory used in NVIDIA and AMD AI accelerators. Samsung, SK Hynix, and Micron, the world's three largest memory manufacturers controlling roughly 90-95% of DRAM production, have responded by pivoting their limited clean room space and capital expenditure toward higher-margin enterprise-grade components.

This is a zero-sum game. Every wafer that becomes an HBM stack for an AI accelerator is a wafer that does not become a stick of desktop RAM or a NAND flash module for a smartphone or SSD. By early 2026, HBM alone was consuming approximately 23% of global DRAM wafer capacity, a share that would have been near zero three years earlier. The simultaneous pivot by some manufacturers toward converting NAND production lines to DRAM, to capture even higher margins in AI-driven markets, has created a cascading scarcity that stretches from server storage to consumer laptops.

The most visible and financially significant consequence of this cascade is that it has removed the ability of even the most powerful consumer electronics buyers to negotiate component costs down to manageable levels.

| Company | Pricing Action | Date | Memory Component Driver |

|---|---|---|---|

| Apple | Mac/iPad up to $300 price hike | June 25, 2026 | NAND up 90%+ QoQ; DRAM up 90-95% Q1 2026 |

| Apple | iPhone 18 Pro expected ~$200 hike | September 2026 (est.) | 256GB NAND: $13 → ~$51 per unit |

| Microsoft | Surface Pro 13-inch: $999 → $1,499 (~50%) | June 2026 | DRAM shortfall from AI wafer reallocation |

| Microsoft | Xbox console price increases | June 2026 | Memory chip squeeze spreading to gaming |

| AWS | Cloud service pricing up ~20% | 2026 | Scarcity costs passed to enterprise customers |

| Dell | Warned of "never witnessed" cost escalation | Nov 2025 | DRAM, HDD, NAND tightening across server line |

Tim Cook described the memory shortage in a Wall Street Journal interview as a "hundred-year flood," something he had never witnessed in more than 40 years in the industry. That statement from the leader of a company with arguably the most sophisticated supply chain management operation on earth is not the language of a cyclical wobble. It is the language of structural disruption.

Why SanDisk's Position Is Different From Other Memory Plays

SanDisk is frequently described in analyst notes as the "pure-play" NAND option, and it's worth explaining precisely what that means in practical terms, since it changes how the company experiences the current supercycle compared to more diversified peers.

When SanDisk completed its spin-off from Western Digital in February 2025, it was separated from the HDD business that had historically dragged on NAND's valuation multiple through what analysts call a conglomerate discount. Freed from the income statement structure of the HDD business, the market was able to value SanDisk based on a pure-play NAND supplier pricing model. This re-rating alone explains a portion of the stock's extreme performance.

But the more operationally significant distinction is the LTA structure. The company has secured five multi-year AI-focused supply agreements worth approximately $42 billion in total commitments. New manufacturing facilities from Micron and SK Hynix are not expected to reach volume production until 2027 at the earliest, meaning SanDisk's contracted customers are locking in supply at elevated prices across a window when the company's entire 2026 production capacity is already sold out.

| Memory Supplier | NAND Pure-Play | Key AI Differentiator | LTA Contract Visibility | US-Listed |

|---|---|---|---|---|

| SanDisk (SNDK) | Yes | Pure NAND, $42B LTA backlog, HBF pipeline | Highest disclosed | Yes |

| Micron (MU) | No (DRAM + NAND + HBM) | HBM growth, diversified | Moderate | Yes |

| Samsung | No (DRAM + NAND + HBM + consumer) | HBM4 development, scale | Limited (not US-listed) | No |

| SK Hynix | No (HBM dominant) | HBM market leader (58% share) | Limited (not US-listed) | No |

| Kioxia | Yes (NAND-focused) | SanDisk JV partner | Not US-listed | No |

Bernstein's argument for the $3,000 target centers on this LTA advantage over Micron. Both companies are beneficiaries of NAND pricing strength, but Micron's more diversified structure means it also carries exposure to DRAM and HBM competitive dynamics, while SanDisk's full concentration on NAND, combined with its contracted revenue pipeline, makes its near-term earnings trajectory more predictable and arguably less subject to the spot-price volatility that characterizes the memory industry's historical boom-bust pattern.

Big Tech's Margin Panic: What the Earnings Call Transcripts Reveal

The degree to which NAND and DRAM cost inflation has become a central concern in 2026 earnings conversations is remarkable. Multiple major technology companies have moved from generic "supply chain awareness" language in 2025 to explicit, detailed warnings about memory cost trajectories in 2026.

Dell Technologies COO Jeff Clarke stated during a late 2025 analyst call that the company had "never witnessed costs escalating at the current pace," describing tighter availability across DRAM, hard drives, and NAND flash memory. A hardware executive from a major PC manufacturer, in a February 2026 analyst call, described "increased input costs driven primarily by the rising prices of DRAM and NAND" and warned that "this volatility is likely to remain throughout fiscal '26 and into fiscal '27." Gartner projected that rising memory prices would make low-margin entry-level laptops under $500 financially unviable within two years. One industry analyst, assessing the magnitude of the shift, described it as "the most significant disconnect between demand and supply in terms of magnitude as well as time horizon" in 25 years of industry experience.

Morgan Stanley noted that memory prices have climbed sixfold over the past year, with new manufacturing capacity likely to take years to build and ramp. JPMorgan analysts estimate DRAM and NAND could jump from roughly 10-15% of an iPhone's total component cost today to more than 45% by 2027. Research firm TechInsights, tracking individual components, estimates the 12GB DRAM package in an iPhone Pro has risen from approximately $39 to a projected $145, a 272% increase for the same quantity of the same chip type. Every one of these disclosures, coming from companies that are motivated to minimize public alarm about their own cost pressures, functions as an involuntary validation of SanDisk's pricing power.

| Analyst/Agency | Memory Price Forecast | Duration | Key Metric |

|---|---|---|---|

| S&P Global Ratings | Elevated through 2028 | Multi-year | AI data center capex persists |

| Morgan Stanley | Sixfold increase in past year | Ongoing | New capacity years away |

| TrendForce | NAND +90% QoQ (early 2026); further +40-50% Q3 | 2026 | Pricing power confirmed |

| IDC | NAND supply growth 17% vs 20-30% historical | Full year 2026 | Below-norm supply growth |

| JPMorgan | DRAM/NAND from 10-15% to 45% of iPhone BOM by 2027 | Into 2027 | Consumer device inflation |

| McKinsey | $7T data center spending through 2030 | Multi-decade | $5.2T AI-focused |

SanDisk's Financial Performance: Reading the Numbers Behind the Stock

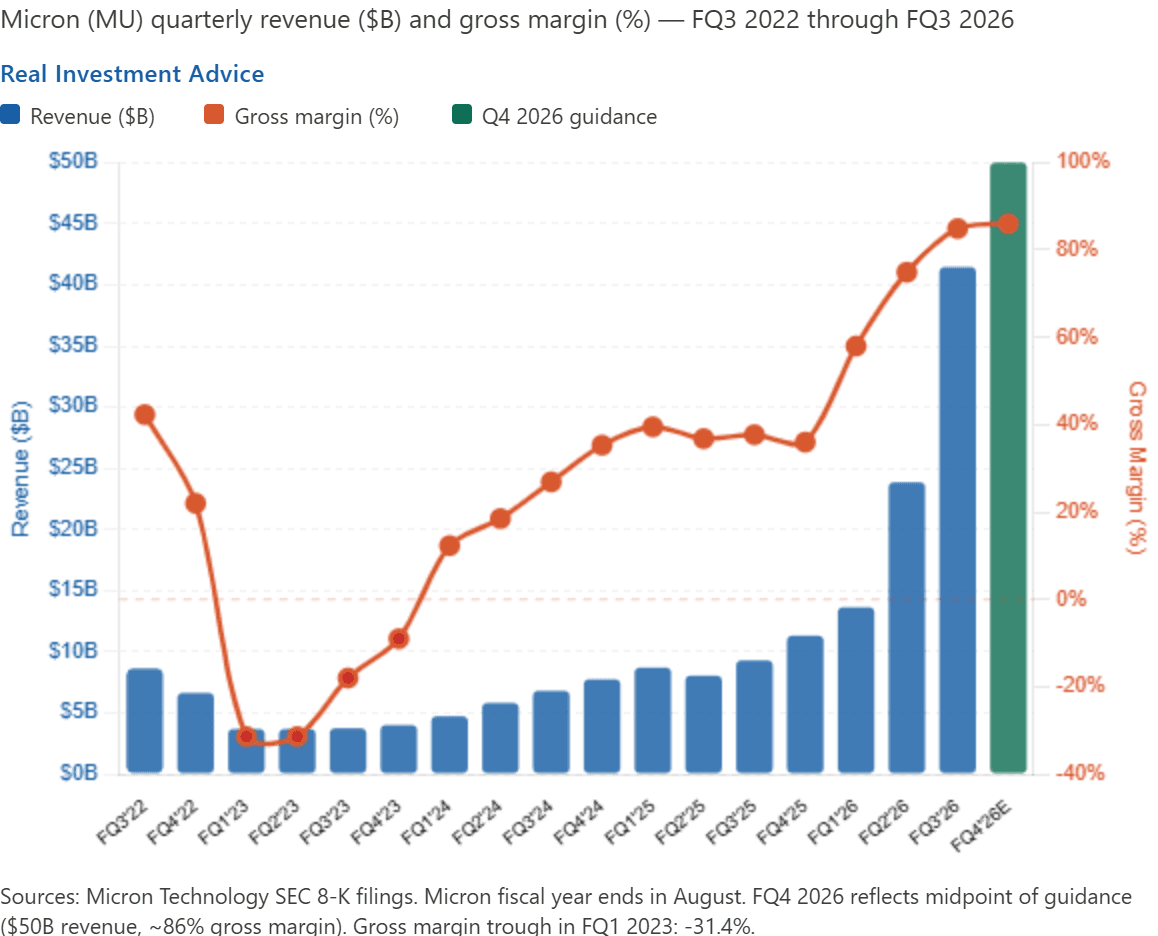

Against this backdrop, SanDisk's most recent quarterly results show a company that is operating almost ideally within the supercycle conditions described above. Fiscal Q3 2026 revenue came in at $5.95 billion, up 251% year-over-year and 97% sequentially, surpassing the company's own guidance range and decisively beating Wall Street estimates. Non-GAAP diluted EPS came in at $23.41, representing a massive beat against analyst expectations of approximately $14, with a positive EPS surprise of nearly 60%. Gross margin expanded by 55.7 percentage points year over year, directly driven by the pricing power generated by the NAND supply shortage. The company's data center segment surged 233% sequentially, and the company ended the quarter completely debt-free, with a $6 billion share repurchase program authorized.

At the Mizuho 2026 Technology Conference, SanDisk highlighted the pace of its revenue trajectory: fiscal 2025 revenue at approximately $7 billion, fiscal 2026 revenue discussed at approximately $20 billion, and Street consensus for fiscal 2027 near $45 billion. This six-fold revenue expansion in roughly three fiscal years, occurring alongside gross margin expansion rather than compression, is the financial architecture that makes even aggressive analyst price targets defensible in forward-earnings terms.

| Metric | Q3 FY2026 Actual | Year-Over-Year Change | Analyst Beat |

|---|---|---|---|

| Revenue | $5.95 billion | +251% | Above guidance |

| Non-GAAP EPS | $23.41 | From -$0.30 loss | ~60% beat vs $14 est. |

| Gross Margin (GAAP) | +55.7pp YoY expansion | Multi-decade highs | Above estimates |

| Data Center Revenue | Surged 233% sequentially | Explosive | Above estimates |

| Net Debt | Zero (debt-free) | Structural improvement | Positive signal |

| LTA Backlog | ~$42 billion | New contracts added | 5 multi-year AI agreements |

The Supercycle vs. Bubble Debate: Two Legitimate Views

The "supercycle debate" framing in this article's title is not just rhetorical. There is a genuine, well-argued disagreement among analysts about whether the current NAND pricing environment represents a durable structural shift or an overextended cyclical peak that will correct sharply when new supply arrives.

The bull case rests on the permanence of AI infrastructure demand, the multi-year timeline for new fabrication capacity (Micron and SK Hynix facilities not reaching volume until 2027 at earliest), the LTA contract structure that locks in elevated pricing beyond spot fluctuations, McKinsey's $7 trillion data center spending forecast through 2030, and the demonstrated willingness of Big Tech buyers to sign contracts that insulate suppliers from spot volatility at the cost of volume commitment.

The bear case rests on the historical pattern of NAND cyclicality, where every upcycle has been followed by an overcorrection as manufacturers simultaneously expand capacity in response to high prices. The analysis from the 2026 global memory manufacturer ranking noted that Kioxia and SanDisk are enjoying premium pricing at the peak of the NAND upcycle but will also face the steepest declines when the cycle reverses. Morgan Stanley's historical modeling, based on the 2016-2018 cycle, predicts industry median gross margins could fall 60% from peak and EPS could come in below consensus by 11%, potentially triggering significant multiple contraction.

Both views are legitimate. The intellectually honest position is that the current AI-driven NAND cycle has structural features, the AI infrastructure buildout, the wafer reallocation dynamic, the long-term contract structure, that did not exist in previous cycles, while also carrying the same fundamental risks that have characterized memory chip investing for decades.

What "SanDisk's NAND Advantage" Actually Means and Its Limits

The headline framing of "NAND monopoly" requires careful qualification. SanDisk is not a monopoly in any regulatory sense. Samsung maintains the largest global NAND market share, and the global NAND market involves at least five significant manufacturers including Samsung, SK Hynix, Micron, Kioxia, and SanDisk itself. What SanDisk possesses is not monopoly power but market positioning advantages that are specific to the current moment: it is the only major US-listed, debt-free, pure-play NAND producer with a disclosed $42 billion LTA backlog, a roadmap technology in HBF that could expand its addressable market, a valuation re-rating freed from HDD conglomerate discount, and a revenue trajectory that the Street is projecting at $45 billion for FY2027.

These are real advantages that translate into real pricing power and earnings visibility. They are not permanent structural advantages that guarantee SanDisk will remain insulated from cyclical forces indefinitely. When new NAND fabrication capacity comes online globally in 2027 and 2028, when Samsung potentially recovers from its current market share disadvantage in AI-grade NAND, and when the supply-demand balance eventually normalizes, the pricing power currently reflected in SanDisk's 55-78% gross margins will face genuine pressure.

The key question for investors and traders is whether the duration and depth of the current cycle's contracted revenue stream is long enough and large enough to justify current valuations, and whether management executes its HBF roadmap on schedule to open the next chapter of margin expansion before the current NAND cycle peaks.

Final Thoughts

Big Tech's margin panic in 2026 has done something that no analyst note could accomplish alone: it has transformed the AI memory supercycle from a semiconductor industry narrative into a consumer-facing, headline-generating reality. When Apple calls memory cost inflation "unavoidable," when Microsoft raises its Surface Pro by 50%, when AWS passes scarcity costs directly to enterprise cloud customers, and when S&P Global Ratings formally forecasts these conditions persisting through 2028, the question of whether the supercycle is real has been conclusively answered by the companies with the most to lose from admitting it. What remains genuinely open is whether it lasts long enough to deliver the full $3,000 price targets implied by Bernstein's most bullish projections, and whether the cycle's eventual reversal arrives before or after SanDisk's HBF technology creates a new layer of structural pricing power. Those questions will likely be answered across the next 12-18 months of earnings reports, NAND contract pricing updates, and new manufacturing capacity ramp announcements. In the meantime, the fundamental debate has shifted from "is this real?" to "how long does it last?" and that is, by most analytical standards, a significantly stronger starting point for the bull case than where the argument was a year ago.

The AI memory supercycle is creating tradeable, high-impact moves across the semiconductor and storage sector. If you want to position yourself ahead of the next SNDK earnings catalyst, monitor NAND pricing updates as they flow through sector reports, or track the broader AI infrastructure trade in real time, sign up through WEEX and start turning your research into action today.

Frequently Asked Questions

1. What is the AI memory supercycle, and is it different from past memory cycles?

The AI memory supercycle refers to the current multi-year period of elevated NAND and DRAM pricing driven primarily by hyperscaler demand for AI data center storage and memory. What distinguishes it from previous cycles is that this shortage stems from a deliberate, structural reallocation of wafer capacity toward high-bandwidth memory for AI accelerators, rather than from demand overshooting supply temporarily. Long-term supply agreements between SanDisk and hyperscalers, totaling approximately $42 billion, also provide a contracted pricing floor that historically was not present in memory downturns.

2. Why does Apple raising its prices confirm SanDisk's pricing power specifically?

Apple is widely regarded as the most powerful supply chain negotiator in consumer electronics. When a company that has historically absorbed component cost swings rather than passing them to consumers announces that price hikes are "unavoidable," it confirms that the NAND pricing environment is beyond the reach of even the most resourceful buyer to negotiate down. For SanDisk, as a pure-play NAND supplier with fully sold-out 2026 capacity, this confirmation directly validates the supply constraint thesis behind its long-term agreement pricing structure.

3. What is the difference between SanDisk and Micron as AI memory investments?

SanDisk is a pure-play NAND flash company with no DRAM, HBM, or HDD exposure, while Micron is diversified across DRAM, NAND, and high-bandwidth memory. SanDisk's concentration means greater earnings sensitivity to NAND pricing swings in both directions, while Micron's diversification provides more buffer across different memory product cycles. Bernstein specifically cited SanDisk's LTA structure as giving it a contract-pricing advantage over Micron in the current environment.

4. How long will the NAND price supercycle last?

Multiple independent forecasts project the shortage extending well beyond 2026. S&P Global Ratings forecasts elevated memory prices through at least 2028, citing continued AI data center investment from Microsoft, Google, Amazon, and Meta. New fabrication capacity from Micron and SK Hynix is not expected to reach volume production until 2027 at the earliest, and McKinsey projects $7 trillion in data center spending through 2030, with $5.2 trillion AI-focused, meaning demand-side pressure is unlikely to abate quickly.

5. What are the risks of investing in SanDisk based on the AI memory supercycle thesis?

The primary risks include the historical cyclicality of the memory chip industry, which has historically seen sharp oversupply corrections after every pricing peak; a stretched valuation at 64-71x earnings versus an industry average of roughly 44x; manufacturing dependency on the Kioxia joint venture; potential faster-than-expected competitive capacity additions from Samsung and SK Hynix; a consumer segment already showing 10% sequential revenue decline; and the possibility that AI capital expenditure slows faster than current hyperscaler guidance implies, reducing the structural demand underpinning the LTA contract values.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. All data, price targets, earnings figures, and industry forecasts referenced in this article reflect publicly available information as of late June through early July 2026 and are subject to change without notice. SanDisk (SNDK) has exhibited extreme price volatility and past performance is not indicative of future results. Analyst price targets, including Bernstein's $3,000 target, represent third-party opinions and are not guarantees of future stock price performance. All investment decisions carry risk of partial or total loss. Always conduct independent research and consult a licensed financial professional before making any investment decision. Neither the author nor the publisher accepts liability for losses resulting from reliance on this content.